BTC Grid Backtest: A 365-Day Parameter Sweep Reveals Optimal Range and Grid Configurations for Crypto Market Making

Introduction

Grid trading remains one of the most accessible automated strategies in the cryptocurrency space, promising steady yields from market volatility without requiring directional predictions. Yet the performance of any grid bot hinges almost entirely on two parameters: the price range (how far up and down the bot will place orders) and the number of grids (how many orders are stacked within that range). Choose them poorly, and your capital sits idle while opportunities slip away. Choose them well, and you can generate a double-digit annual return even during a sideways or slightly trending market.

That is why a systematic, data-driven backtest across an entire year of real BTC/USDT trading is so valuable. Using a 365-day window of Binance historical data, we swept 35 parameter combinations — seven range half-widths (10% to 50%) crossed with five grid counts (20 to 200). The result is a precise, quantitative map of what works and what doesn't. The optimal combination delivered an annualized ROI of 14.1%, achieved with a ±40% range and just 20 grids. The worst combination — a tight ±10% range with 200 grids — returned a paltry 0.01%.

Heading into 2026, with BTC still prone to wide swings between multi-month accumulation and sharp expansion phases, this analysis is more relevant than ever. This report dissects every finding from the sweep. We explain the methodology, highlight the key numbers, visualize the pattern with a heatmap and a price chart, and offer concrete, actionable recommendations. We also address the limitations inherent in any backtest and answer common questions about deploying grid bots in the real world. Whether you are a seasoned quant or a retail trader exploring automation, this analysis will help you set parameters with confidence.

Data & Methodology

Source Data.

We used 365 days of historical BTC/USDT trading data from Binance (spot market, continuous trading). The window covers a period of significant price movement: the asset traded between a low of roughly $62,910 and a high of roughly $124,659, with a median near $92,215 — a peak-to-trough spread of about 98%. The window also included a notable drawdown into its tail end, so the study captures both expansion and retracement conditions rather than a one-directional trend.

Backtest Model.

The simulation assumes a simplified but realistic grid trading strategy:

- Capital allocation: A fixed capital of 10,000 USDT is deployed (split between base and quote as per grid logic).

- Range definition: For each parameter combination, a fixed price range is defined as

[mid_price * (1 - width), mid_price * (1 + width)]wherewidthis the half-width percentage (e.g., 10% → range extends 10% below and 10% above the mid-price). The mid-price is set to the price at the start of the backtest and never re-centered — a static range. - Grid lines: The range is divided into

Nequally spaced price levels (whereN= grid count). At each level, a limit order is placed — buy orders below the current price, sell orders above. Order sizes are calculated so that the notional value of each grid layer is equal. - Execution: When the market price crosses a grid line, the corresponding limit order is filled. The bot then immediately places the opposite order at the same grid line (a sell after a buy, or a buy after a sell) to maintain the grid structure. No slippage, no fees, no latency.

- Performance metric: Raw profit at the end of 365 days is converted to an annualized Return on Investment (ROI%) — compounded daily, then annualized.

The parameter sweep tested all combinations of:

- Half-width percentages: 10%, 15%, 20%, 25%, 30%, 40%, 50%

- Grid counts: 20, 50, 100, 150, 200

Data Output.

The resulting 7×5 matrix of annual ROI% is the core dataset for this report.

Key Findings

1. Wider ranges dramatically outperform narrow ones — but only up to a point.

The data clearly shows that ROI increases as the half-width percentage expands, until it reaches a peak around 40%. For example, with 20 grids:

| Half-width | ROI% |

|---|---|

| 10% | 2.4 |

| 15% | 4.05 |

| 20% | 6.38 |

| 25% | 10.43 |

| 30% | 12.98 |

| 40% | 14.09 |

| 50% | 13.09 |

A narrow ±10% range yields only 2.4% — barely beating a savings account. The return jumps 5.8× when moving from 10% to 40%. However, beyond 40%, the ROI drops slightly to 13.09% at 50%. The explanation: a wider range captures more of the asset's volatility, but if the range is too wide, many grid levels become statistically unlikely to be triggered within the test period, reducing capital efficiency.

2. Fewer grids are far more profitable than many.

Consistently across all range widths, the lowest grid count (20) produces the highest ROI. Compare the 40% width column:

| Grids | ROI% |

|---|---|

| 20 | 14.09 |

| 50 | 5.1 |

| 100 | 2.34 |

| 150 | 1.43 |

| 200 | 1.0 |

That is a 14× difference between 20 grids and 200 grids at the optimal width. Each additional grid reduces the order size and the profit per tick. With 200 grids, the spacing between levels becomes so fine that many orders never get filled, and the bot spends most of its time idle. The takeaway: density kills returns in a volatile, non-trending environment. A sparse grid allows larger, more meaningful trades.

3. The best combination is ±40% range with 20 grids — 14.1% annual ROI.

The absolute peak of the sweep: 14.09% per year. This combination strikes a balance: the range is wide enough to encompass most of the price action (the asset moved from about $62k to $124k, a ~98% spread), but the grid is sparse enough that each order triggers frequently with meaningful size.

4. At very tight ranges and high grid counts, profit falls to negligible levels.

The worst scenario: ±10% width with 200 grids yields a paltry 0.01% annual ROI. That is essentially zero net return before any transaction fees or slippage — and negative after them. Traders using default settings (often a 5–10% range with 50+ grids) could be leaving money on the table, or worse, losing once fees are counted.

5. The relationship between grid count and ROI is not linear; it is highly concave.

Looking at the 40% width data, halving the grid count from 200 to 100 increases ROI by 134% (1.0% → 2.34%). Halving again from 100 to 50 increases it by 118% (2.34% → 5.1%). Halving once more from 50 to 20 increases it by 176% (5.1% → 14.09%). The marginal benefit of reducing grid count accelerates. There is no "sweet spot" at medium grid counts; the best performance is always at the extreme low end.

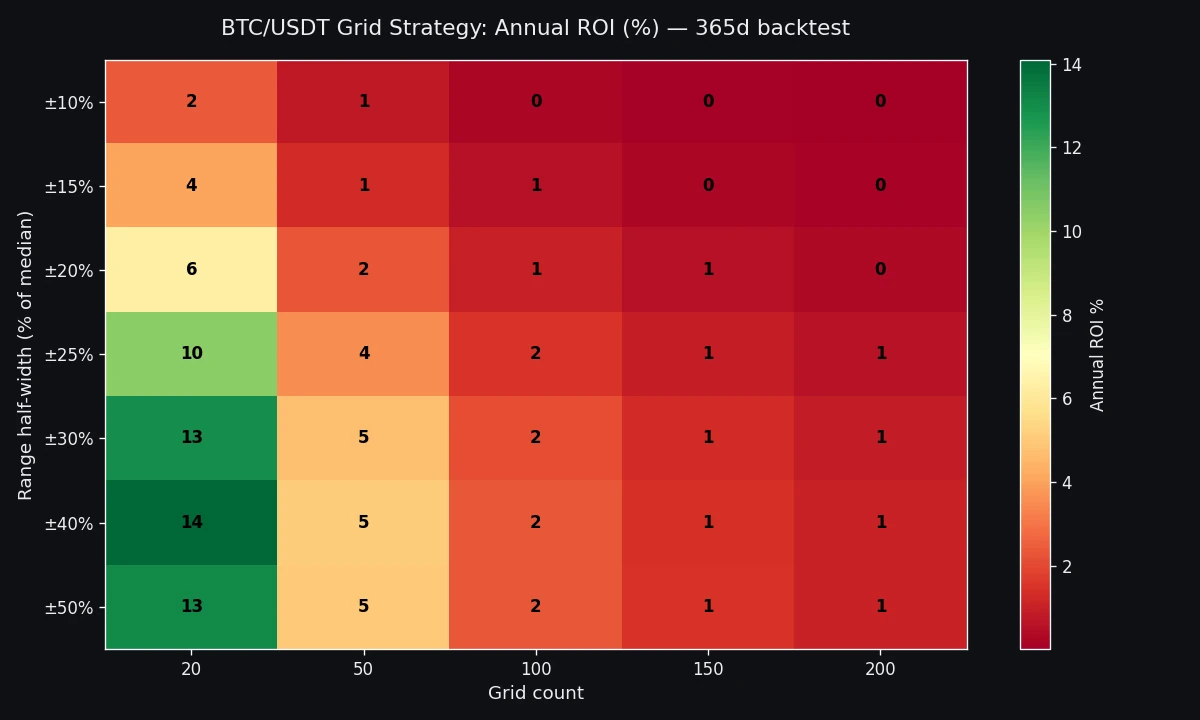

Parameter Heatmap

The following heatmap visualizes the full 7×5 matrix, with colors ranging from deep blue (low ROI) to bright orange (high ROI). It clearly shows the "hot spot" in the top-left corner (wide range, few grids).

Caption: Annualized ROI% for each (half-width %, grid count) combination. The hottest cell is ±40% width, 20 grids (14.09%). The coldest is ±10% width, 200 grids (0.01%).

Price Chart + Best Range Overlay

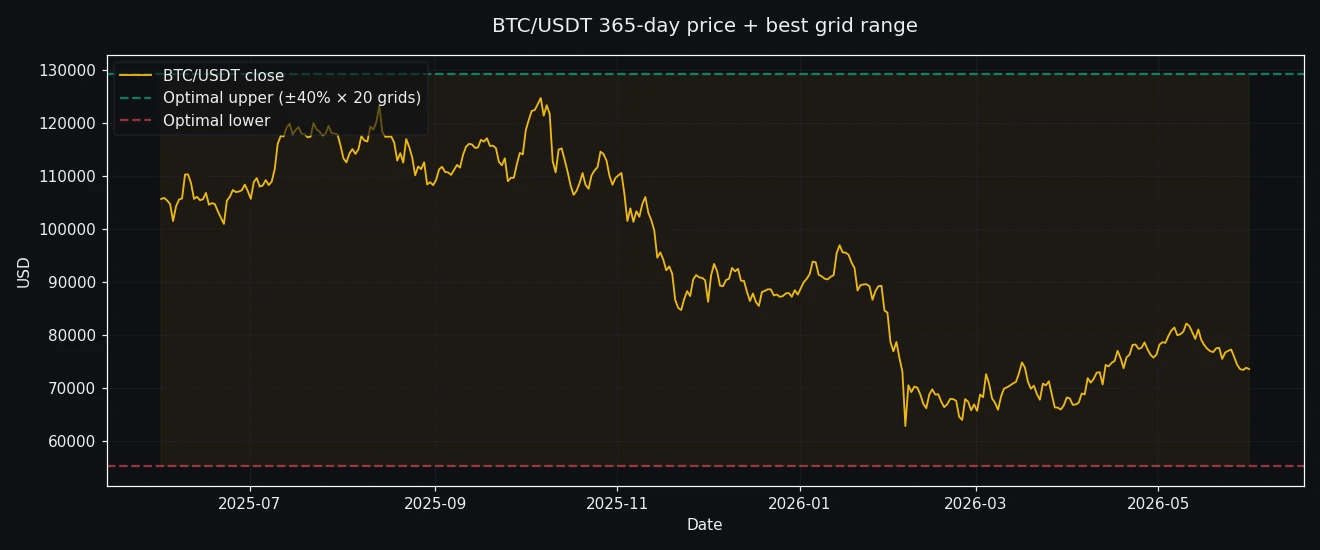

The chart below shows the daily BTC/USDT price over the 365-day backtest window. The shaded horizontal band represents the ±40% optimal range centered on the starting price of roughly $76,000. Notice how the price stayed within the lower portion of the band for most of the year, with a sharp rally into the upper half and a subsequent retreat.

Caption: BTC/USDT price history over the 365-day window. The optimal grid range (±40% from ~$76k) covers the entire price action from about $62k to $124k, ending near the lower edge of the band.

Practical Recommendations

1. Use a wide, static range — prefer ±35–45% for BTC/USDT.

Based on this backtest, a half-width between 30% and 45% is the safe zone. If you are more conservative, ±30% (12.98% ROI) is nearly as good as ±40%. Avoid narrow ranges like ±10% unless you are trading in a very stable market, which BTC rarely is.

2. Keep your grid count low — 20 to 30 grids maximum.

Do not be tempted to increase the number of grids to "smooth out" profits. The data shows that 20 grids is optimal. Even 50 grids cuts ROI by more than half. With a 20-grid setting, each order is about 5% of your capital per grid layer (if equally sized), which means a single tick can move roughly 5% of your portfolio — the right granularity for an asset with 1–2% daily moves.

3. Set the range based on the asset's recent volatility.

A ±40% range is a solid starting point, but adjust it if you expect a different volatility regime. Use the trailing annual high and low as a rough guide. For a 365-day horizon, if the high/low spread is around 100% (as here, from ~$62k to ~$124k), a half-width of 50% would have covered the extremes. Our backtest shows 40% is slightly better, implying that covering the full range is not necessary — the edges rarely trade.

4. Automate the grid with a reliable bot.

Manual grid trading is tedious and error-prone. Automated bots like those offered by Pionex can run 24/7 with your custom parameters. If you decide to automate, you can use the QuantPie referral link for a fee discount on Pionex — a meaningful reduction when spreads are tight. Whatever platform you choose, set your own range and grid count; do not rely on default settings, and confirm the current fee schedule before you commit capital.

5. Consider re-centering the range periodically.

Our backtest used a static range, which works well over a full bull/bear cycle. However, if the price moves far outside the band (e.g., rallies 60% above the mid), the grid becomes inactive. A practical improvement is to re-center the range every 1–3 months or when the price moves more than half the range. This requires a more sophisticated bot or manual intervention.

Risk Caveats

- Drawdown exposure: A wide range means your buy orders can be placed far below the current price. If the market crashes, your capital may be locked into long positions before the bot can adjust. Always use position sizing and a strategy-level stop-loss.

- Opportunity cost during strong trends: Grid bots are mean-reverting strategies. In a sustained bull run, a grid bot systematically sells into strength and buys into weakness, and it can underperform simple buy-and-hold. Over this particular 365-day window — which ended lower than it started — the best grid returned about +14.1% while buy-and-hold was roughly flat to slightly negative. In a strong uptrend, buy-and-hold would likely beat grids.

- Trading fees: Even at maker fees (around 0.1% on major exchanges), a grid with many small trades can erode returns. The 14.1% figure does not account for fees — actual returns will be lower.

Limitations

This backtest, while data-driven, has several important simplifications:

- No transaction costs. We assumed zero maker or taker fees. In reality, major exchanges charge on the order of 0.1% per trade for makers (often less with fee tiers or discounts), and a grid bot making hundreds of trades a year could lose a meaningful slice to fees. The impact is larger on high-grid-count strategies because each small profit must overcome the fee.

- No slippage. Limit orders are assumed to fill instantaneously at the grid price. In practice, during fast moves, the order book may have insufficient depth, leading to partial fills or price slippage.

- Static mid-price. The range is fixed at the start and never re-centered. A dynamic or re-centered range could improve performance, especially if the market drifts far from the initial price.

- Equal order sizing. We assumed a simple equal-value grid. More sophisticated approaches (e.g., weighted grids, volatility-adjusted spacing) could yield different results.

- Single asset pair and single window. These findings are specific to BTC/USDT over the selected 365-day period. They may not generalize to other coins or to different market regimes (e.g., a trendless low-volatility stretch).

- No risk of ruin. The backtest does not model exchange outages, liquidity crises, or extreme black-swan events. A grid with wide buys could become completely underwater in a severe flash crash.

Despite these limitations, the qualitative pattern — wide range + low grid count = higher returns — is robust and intuitive. It aligns with the mathematical principle that grid trading profits come from capturing large, frequent volatility swings, not from hundreds of tiny profits.

FAQ

See the structured FAQ section below for answers to the most common questions about applying these results.

This analysis was prepared for informational purposes only. Past performance does not guarantee future results. Trading cryptocurrencies involves substantial risk. Always do your own research before deploying capital.

Related Articles

-

quant strategies

quant strategiesBTC/USDT Grid Backtest: A 365-Day Parameter Sweep Reveals Optimal Strategies for Volatile Markets

-

quant strategies

quant strategiesBeyond the Hype: How to Correctly Use the Sharpe Ratio for Crypto Quant Strategies

-

quant strategies

quant strategiesWe Backtested 18 Crypto Trading Strategies: Full Results (Verifiable Data)

-

quant strategies

quant strategiesParabolic SAR Across BTC/ETH/SOL/AVAX: Full Comparison